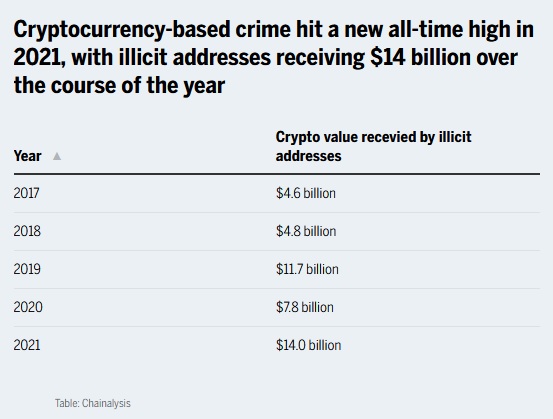

At the start of 2022, illegitimate addresses contained a minimum of $10 billion in bitcoin, the great bulk of which was retained by wallets linked to cryptocurrency crime. Addresses linked with darknet marketplaces and frauds also play a big role in this number. Nevertheless, the proportion of fraudulent trades as a proportion of bitcoin trading volumes fell to a historic low of 0.15% last year, notwithstanding the raw value of illicit activities reaching an all-time peak.

Scamming was the most common kind of cryptocurrency-related offense last year, trailed by theft. Total trading volume among all cryptocurrencies monitored by Chainalysis increased to $15.8 trillion in 2021, up 567% from aggregates in 2020. “It’s no mystery that an increasing number of crooks are utilizing bitcoin, given its rapid growth. The reality that the growth was a mere 79% — almost a level smaller than total adoption — may have been the most surprising of all. In reality, with legal bitcoin use vastly exceeding unlawful utilization, the percentage of cryptocurrency trading volume accounted for by unlawful activity hasn’t been lower” Chainalysis mentioned.

The majority of bitcoin transmitted from fraudulent wallets usually ends up on popular exchanges. The count of active financial frauds at any moment in the year increased dramatically to 3,300 in 2021, from 2,052 in the earlier year. A monetary scam’s average lifetime is becoming shorter and shorter. According to Chainalysis statistics, the typical financial fraud remained operational for a mere 70 days in 2021, a decrease from 192 in 2020.

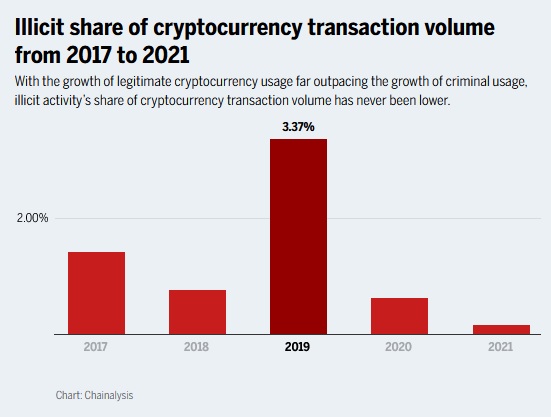

Yearly statistics show that unlawful activities are becoming a lesser component of the cryptocurrency environment — with the exception of 2019, which was an anomaly year owing mostly to the PlusToken Ponzi scam. They also demonstrate the evolution of legal enforcement’s abilities to tackle cryptocurrency-centered criminality.

The CFTC charging multiple investment schemes, the FBI taking down the notorious REvil ransomware strain, and OFAC punishing Suex and Chatex, two Russia-headquartered cryptocurrency firms significantly implicated in money laundering, are just a few cases. The IRS Criminal Investigation division seized about $3.5 billion in bitcoin from non-tax scrutiny in November 2021.

Nevertheless, two kinds of cryptocurrency crimes stood out with respect to growth: stolen assets and frauds. Decentralized finance (DeFi) was a significant component of both, with DeFi trading volumes increasing tenfold by 2021. DeFI enables crypto-denominated loans outside of conventional banks, and it has been a major contributor to the rise in stolen assets and frauds.

In 2021, DeFi transaction volume increased 912%, according to Chainalysis, and amazing returns on decentralized tokens such as Shiba Inu have prompted investors to bet on DeFi tokens. “DeFi is among the most interesting sectors of the bitcoin ecosystem, offering tremendous opportunity to both businesses and cryptocurrency consumers However, DeFi’s full promise is doubtful to be realized if the highly praised decentralization paves way for for rampant embezzlement. Improved coordination is one approach to address this; both the commercial and governmental sectors can play an essential role in educating investors on how to avoid risky initiatives. In the years to come, the crypto sector may need to adopt more serious measures to avoid tokens affiliated with potentially deceitful or dangerous ventures from being published on large exchanges” Chanalysis stated.

Scamming earnings increased by 82% to $7.8 billion last year with cryptocurrencies looted from victims. Rug pulls, a pretty modern scam style in which developers establish what look to be real cryptocurrency ventures, implying they do far more than merely establishing wallets to collect bitcoin for, instance, bogus investment possibilities — before taking customers’ money and vanishing.

Approximately 90% of the entire value lost through rug pulls in 2021 may be linked to one bogus centralized crypto exchange, Thodex, whose CEO vanished shortly after the exchange suspended customers’ ability to withdraw assets. Almost every rug pull documented by Chainalysis in 2021, on the other hand, featured DeFi initiatives.

“In virtually all of these instances, initiative owners duped investors into buying tokens linked with a DeFi venture before emptying the resources provided by those backers, thereby reducing the token’s value to zero” Chanalysis concluded. In terms of bitcoin theft, $3.2 billion in cryptocurrencies was plundered in 2021, a 516% increase over the previous year.

Approximately $2.2 billion of the monies, or 7% of the amount for 2021, were stolen via DeFi protocols. Unfortunately, DeFi protocols had the greatest increase in adoption for money laundering at 1,964% increase.